The Volta Foundation have recently released the 2025 edition of their annual Battery Report. These open-access reports are well-renowned in the battery world and provide a comprehensive analysis of developments in battery research, industry and regulations. We at Mewburn Ellis were delighted to participate in this year’s report, as Senior Associate Chloe Flower co-authored and contributed to the policy section.

This is the fourth article in our 2025 Report series. Following on from our article on IP litigation in the battery sector, we now take a look at the current trends in patent applications being filed in this technical field. Which territories are seeing the most patent activity, which companies are driving this, and which particular technologies are making waves.

Battery innovation at scale: what the 2025 patent landscape tells us

Innovation within the battery industry is thriving. One of the clearest signals of this growth is found by looking at the global battery patent landscape.

Data from the Volta Foundation’s Battery Report 2025 paints a picture of a sector that is both burgeoning with innovation and increasingly congested from an intellectual property perspective. While battery chemistries continue to diversify, the way innovation is protected – where, by whom, and in which technical areas – is becoming more concentrated and strategically nuanced.

Asia leads the way

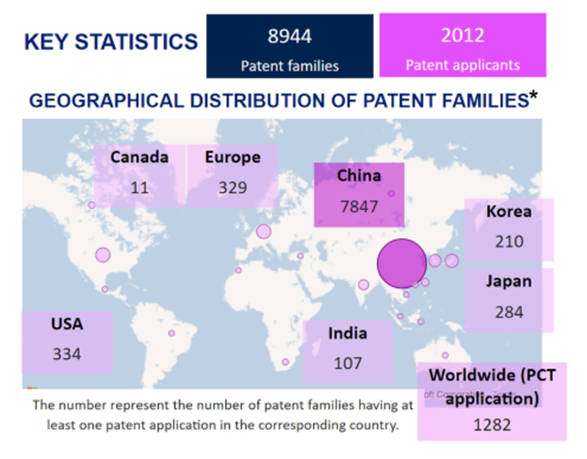

It is no surprise to see China dominating global patent filing activity, but the extent and nature of that dominance in 2025 are striking. China leads the way in the number of patent applications filed in important current and future battery technology areas: including solid-state lithium-ion batteries, sodium-ion batteries (as shown below), zinc-ion batteries, and battery recycling technologies.

Geographical distribution of patent filings in 2025 relating to sodium-ion batteries [taken from page 747 of the report; chart was provided by KnowMade; patent search was done in December 2025 by KnowMade, using keywords and IPC/CPCs (H01M, H02J-007) in Orbit (Questel)]

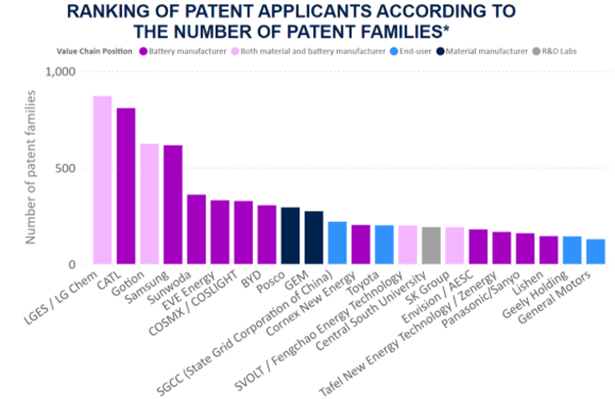

While China is home to some of the biggest players in the battery sector (such as CATL, Sunwoda and Gotion), there is plenty of innovation occurring elsewhere in Asia too. As shown in the chart below, in lithium-ion technology, the companies in first and fourth place for the most patent families in 2025 are South Korean: Samsung and LG Chem. Japan’s Toyota and Panasonic also feature in the top 20. Interestingly, the first company based in the Western hemisphere only appears at 22nd in this list (General Motors).

It appears that the global battery patent landscape is becoming more asymmetric: while Asian companies – particularly Chinese, Korean, and Japanese companies – pursue large, Asia‑centred portfolios, many Western applicants remain more selective in where and how they file.

At the same time, due to the intensity of global patent filing, battery sectors such as lithium- and sodium-ion technologies are becoming increasingly crowded by IP. Commercial freedom-to-operate is therefore becoming a growing challenge for businesses, particularly in Asia. The 2025 Battery Report highlights the importance of patent landscaping, licensing, and enforcement for companies to defend their IP rights and avoid infringing others.

Patent applicants by number of patent families relating to lithium-ion batteries in 2025 (taken from page 744 of the report; chart was provided by KnowMade; patent search was done in December 2025 by KnowMade, using keywords and IPC/CPCs (H01M, H02J-007) in Orbit (Questel))

A shift away from “new chemistry” patents

One of the important trends in the 2025 data is where patenting activity is growing fastest. While active materials – such as cathodes and anodes – remain central, much of the strongest growth appears in what might be described as enabling or system‑level technologies.

Patents relating to battery management systems (BMS), separators, electrolytes, binders, current collectors and cell architecture continue to expand, even as some traditional material categories show slower growth or slight decline. This suggests a maturing field in which competitive advantage is increasingly sought in areas crucial to commercialisation and scale‑up, such as integration, optimisation and reliability, rather than through entirely new chemistries alone.

Li‑ion still dominates - but alternative chemistries are maturing

The data in the report shows that lithium‑ion technologies remain the backbone of global battery innovation. However, the 2025 landscape also shows sustained and sizeable growth in alternative systems.

Sodium‑ion technologies, in particular, continue to gain momentum, with patent growth driven largely by Chinese industrial and academic applicants. Zinc‑based and redox‑flow batteries, while smaller for now in absolute numbers, continue to develop as well (see page 741 of the report).

What is notable is not just the presence of these alternatives, but their persistence. The number of patent filings has increased consistently over several years for many of these technologies, most notably sodium- and zinc-ion batteries. This sustainable growth demonstrates real potential staying power, rather than a temporary academic interest in these alternative battery chemistries.

Recycling and sustainability: growing, but concentrated

Battery recycling continues to attract patent attention, reflecting global sustainability objectives and long-term material security concerns. However, as discussed on page 748 of the report, recycling patents remain highly concentrated geographically and organisationally, with China and a relatively small number of Asian companies accounting for a large share of filings.

With concerns over recycling and the re-use of rare earth minerals found in batteries being a global issue, it will be interesting to see where these technologies are developed and protected in the future.

Looking ahead

The report portrays a battery sector burgeoning with patent filings, particularly in certain geographical areas such as Asia and especially China. The IP landscape is becoming increasingly congested. For companies operating in this space, the challenge is therefore not simply to innovate, but also to traverse the increasingly complex IP environment to protect their innovations and avoid infringing the IP rights of others (which can lead to disputes and potential litigation).

It is essential that companies in this sector treat IP as a core strategic consideration, rather than a legal afterthought. The battery tech team at Mewburn Ellis has deep experience in assisting battery-focused businesses – from start-ups to multinational enterprises – to make the most of their IP and delicately navigate the competitor landscape.

Read the full Battery Report 2025 series here.